Paison Tazvivinga and Irene Bumi

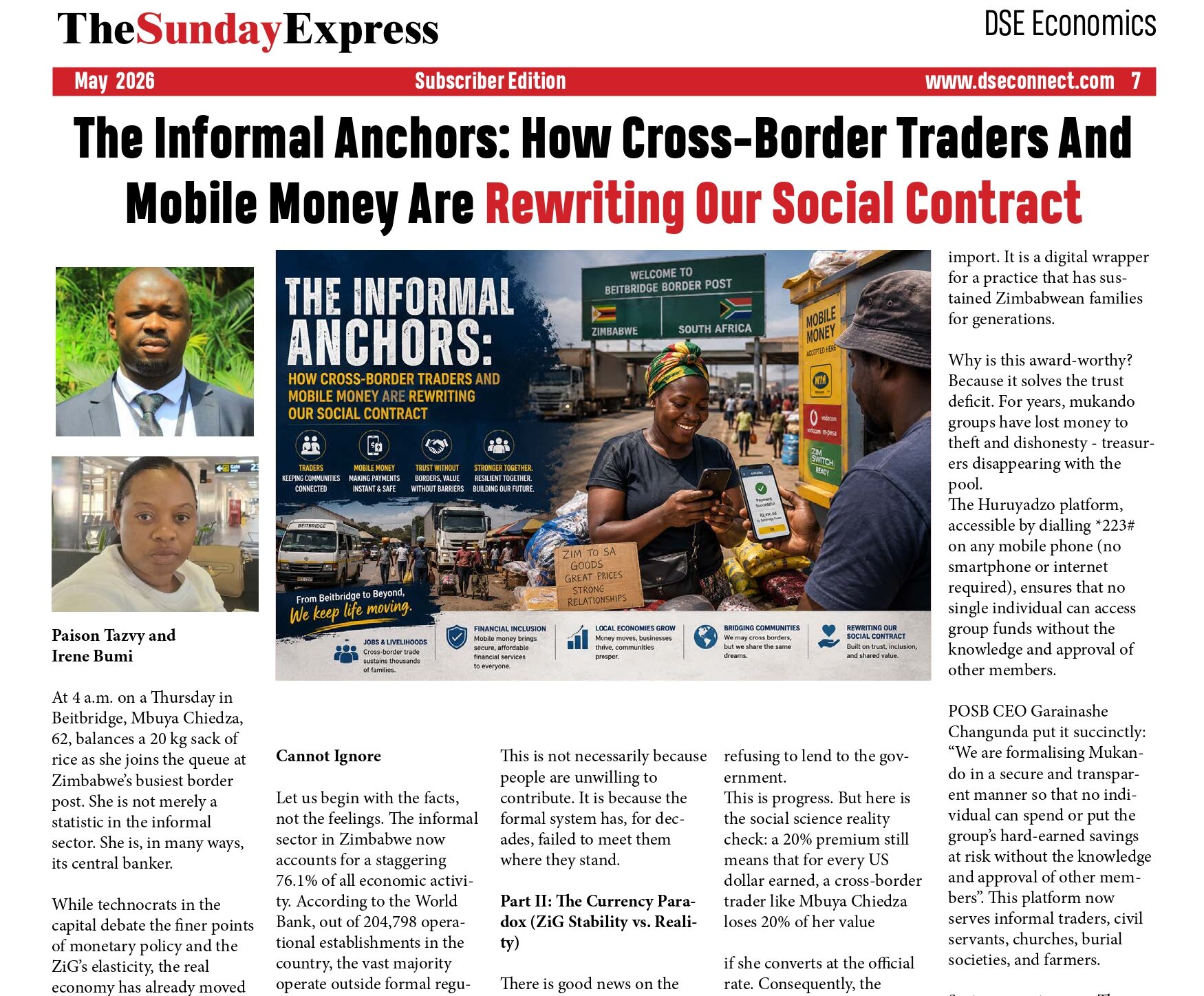

At 4 a.m. on a Thursday in Beitbridge, Mbuya Chiedza, 62, balances a 20 kg sack of rice as she joins the queue at Zimbabwe’s busiest border post. She is not merely a statistic in the informal sector. She is, in many ways, its central banker.

While technocrats in the capital debate the finer points of monetary policy and the ZiG’s elasticity, the real economy has already moved on.

Today, we argue that Zimbabwe’s most resilient economic institutions are no longer found in the boardrooms of Harare but in the mukando savings circles of Mbare and the mobile money wallets of cross-border traders.

A single article cannot capture all the diverse informal sector players. We have chosen Mbuya Chiedza as a lens because cross-border trade sits at the intersection of currency policy, mobile money, gender, and regional commerce – themes central to Zimbabwe’s current economic debate.

However, no single story represents the whole.

Part I: The Numbers We Cannot Ignore

Let us begin with the facts, not the feelings. The informal sector in Zimbabwe now accounts for a staggering 76.1% of all economic activity.

According to the World Bank, out of 204,798 operational establishments in the country, the vast majority operate outside formal regulatory frameworks.

The total value of this shadow economy is estimated at US$39.8 billion relative to GDP.

For the average citizen, this is not a statistic. It is a survival strategy. The Zimbabwe Revenue Authority (ZIMRA) confirms that the informal economy generates approximately US$14.2 billion annually, with an estimated US$2.5 billion in cash circulating at any given time.

Yet, here is the uncomfortable truth for policymakers: only 6% of informal players pay taxes. As World Bank consultant economist Abel Gwaindepi noted recently, taxes are paid by a few – mostly in the goods sector – while service providers remain harder to monitor.

This is not necessarily because people are unwilling to contribute. It is because the formal system has, for decades, failed to meet them where they stand.

Part II: The Currency Paradox (ZiG Stability vs. Reality)

There is good news on the monetary front, and we should acknowledge it. Since the introduction of the Zimbabwe Gold (ZiG) currency in April 2024, the country has experienced a degree of exchange rate stability rarely seen in recent history.

Throughout 2025, the interbank rate averaged around ZiG 26 to the US dollar, with annual ZiG inflation falling to 15% by the end of 2025, and further down to 4.1% in January 2026.

The parallel market premium – that gap between official and street rates – has narrowed significantly, from over 140% in the pre-ZiG era to roughly 20% today. The multicurrency regime has been extended to 2030, and the Reserve Bank has maintained discipline by refusing to lend to the government.

This is progress. But here is the social science reality check: a 20% premium still means that for every US dollar earned, a cross-border trader like Mbuya Chiedza loses 20% of her value

if she converts at the official rate. Consequently, the parallel market – facilitated by WhatsApp groups and mobile money – remains the preferred price discovery mechanism. Until that premium is zero, we will not see mass voluntary formalisation.

Part III: The Mukando Revolution – Formalisation from the Ground Up

This brings us to the most hopeful development of the last several months, one that bridges the gap between economic theory and social practice.

In February 2026, the People’s Own Savings Bank (POSB) launched Huruyadzo/Inkunzi, a mobile-based group savings platform that formalises the traditional mukando (rotating savings club) system. This is not a Western import. It is a digital wrapper for a practice that has sustained Zimbabwean families for generations.

Why is this award-worthy? Because it solves the trust deficit. For years, mukando groups have lost money to theft and dishonesty – treasurers disappearing with the pool.

The Huruyadzo platform, accessible by dialling *223# on any mobile phone (no smartphone or internet required), ensures that no single individual can access group funds without the knowledge and approval of other members.

POSB CEO Garainashe Changunda put it succinctly: “We are formalising Mukando in a secure and transparent manner so that no individual can spend or put the group’s hard-earned savings at risk without the knowledge and approval of other members”.

This platform now serves informal traders, civil servants, churches, burial societies, and farmers.

Savings earn interest. There are no monthly fees. It is, in essence, a bridge between the informal reality and the formal financial system – a bridge built on existing social structures rather than imported blueprints.

Part IV: Beitbridge – The Gateway That Works

While policymakers deliberate, the private sector is voting with its capital. Last month, a new US$1.5 million duty-free shop opened at the Beitbridge Border, with plans to invest a further US$3 million over five years, creating up to 70 local jobs.

This follows a US$300 million modernisation of the border facility by the government and the Zimborders Consortium.

Matabeleland South Minister of State, Cde Albert Nguluvhe, declared: “Beitbridge is no longer just a border. It is a business gateway”.

Simultaneously, Unifreight Africa imported 60 new Swift trucks (part of a 100-unit fleet expansion) specifically to meet growing demand on regional corridors linking Zimbabwe to South Africa, Zambia, and beyond. CEO Richie Clark noted that trade volumes continue to rise, particularly in mining, agriculture, and retail distribution.

These are not speculative investments. They are evidence that the informal trade corridor – the very artery Mbuya Chiedza travels – is robust, growing, and essential to regional commerce.

Part V: The EcoCash Reality and Digital Inclusion

No discussion of Zimbabwe’s informal economy is complete without acknowledging the digital infrastructure that powers it. EcoCash remains the dominant mobile money platform, accounting for over 70% of all national payment transactions and holding 86% of the mobile money market share.

Why does this matter? EcoCash and its competitors (InnBucks, Omari, Mukuru) have done what banks could not: bring financial services to the unbanked. From school fees to ZESA tokens, from diaspora remittances to church payments, the mobile money ecosystem is the circulatory system of the informal economy.

As financial expert Ngoni Dzirutwe observed: “Trust plays a big role in financial services, and EcoCash has built that trust over the years”. That trust is social capital – and it is the most valuable currency we have.

Part VI: A Path Forward – For Policymakers and Citizens

So where do we go from here? We offer three evidence-based recommendations.

First, to the authorities: ZIMRA has already set a target to register over 50,000 new taxpayers in 2026. This is commendable. But registration is not enough. They must offer value in return – security, dispute resolution, and tangible services. The POSB Huruyadzo model demonstrates that formalisation works when it addresses a real problem (theft) rather than merely demanding compliance.

Second, to businesspeople: The future is hybrid. The informal sector is not going to disappear. The smartest investors will partner with it – through mobile money integrations, supply chain linkages, and formalisation programmes that respect existing social structures.

Third, to community members: You are not economic outlaws. You are innovators. The 76.1% is not a problem to be solved. It is a foundation to be built upon. But with innovation comes responsibility. Consider platforms like Huruyadzo that protect your savings. Demand transparency. Build trust.

The Wisdom of Mbuya Chiedza

We conclude where we began.

Mbuya Chiedza does not read monetary policy statements. But she knows that if the official ZiG rate diverges too far from the Beitbridge rate, she will transact accordingly. That is not speculation. That is three decades of survival wisdom compressed into a single economic heuristic.

The question facing Zimbabwe is not whether the informal economy will be formalised. It is whether our formal institutions will have the courage to learn from the systems that already work—the mukando circles, the mobile money networks, and the cross-border corridors.

The 76.1% is not waiting for permission. It is already building the future. The only question is whether we will have the wisdom to join them.

Paison Tazvy is an economist, and Irene Bumi is a social scientist. They can be contacted at ptazvy@gmail.com. This article draws on data from the World Bank (2025), Zimbabwe National Statistics Agency, Reserve Bank of Zimbabwe, POSB, ZIMRA, and field research conducted along the Harare-Beitbridge-Johannesburg corridor.